Global Markets

Tradable Products

You are viewing this site in certification mode

A fundamental risk management technique is to measure the P&L impact of changes to market conditions. Cboe Hanweck Options Analytics' Scenario Analytics content offers you the ability to see how changes in price, volatility and the passage of time will affect individual securities across the complete universe of listed options and futures. The P&L scenarios for each security are delivered in the familiar form of a data feed. The data feed can be easily combined with in-house risk and position management systems thereby protecting sensitive proprietary portfolio information.

For each scenario, you can specify different market conditions for individual securities in an easy-to-understand manner.

Cboe Hanweck Options Analytics' Scenario Analytics is a customizable set of individual scenarios combined into a vector of profit-and-loss calculations delivered as a data feed. Cboe Hanweck does the heavy computational processing and presents the analytics in a familiar and easy-to-integrate format – just like any other data feed.

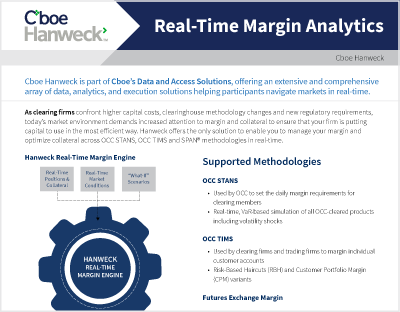

Most exchange portfolio margin calculations are based on scenario analysis techniques – methodologies such as OCC TIMS® and SPAN® are examples. Cboe Hanweck publishes special-case P&L vectors that conform to many exchange margin methodologies.

TIMS®, STANS®, and OCC® are registered trademarks of The Options Clearing Corporation ® (OCC). OCC assumes no liability in connection with the use of STANS or TIMS by any person or entity. The current version of TIMS or STANS may not be reflected in the Cboe Hanweck services described herein.